Big Question

How does political risk (e.g. expropriation) influence the destination of foreign direct investment for multinational enterprises?

Research Question and Contribution

The dissertation contributes to the empirical literature in international business (IB) on the impact of investor–state investment disputes pertaining to foreign direct investment (FDI) flows. It consists of three studies that examine two sets of topics of recurrent interest to IB scholars and practitioners:

-

international risk management and country political and economic risks, especially related to the identification and mitigation of risks associated with FDI (such as government expropriation);

-

business-government relations and links between multinational enterprises (MNEs) and the political/regulatory framework in which they operate.

The dissertation advances our understanding of how MNEs assess investment risks abroad, the role of international arbitration mechanisms in signaling host state credibility, and the domestic public politics of foreign investment attraction. The findings presented below are relevant for scholars, foreign investors, and government officials and policymakers concerned with FDI.

Dissertation Overview

The overall goal of the study is to assess how legal disputes between international investors and countries hosting FDI can shape states’ reputations as safe investment locales and, in turn, their ability to attract FDI. In terms of legal disputes, I focus on investor–state dispute settlement (ISDS) cases. For example, in 2006 a U.S. oil company sued Ecuador for expropriation and, in 2012, the government of Ecuador was ordered to pay around two billion US dollars for damages (Occidental v. Ecuador II, ICSID Case No. ARB/06/11). More generally, UNCTAD reports more than 1,300 ISDS cases to date (Investment Policy Hub). The dissertation consists of three articles and is structured as a multi-method study, with three distinct sources of evidence requiring three different methods of analysis.

In what follows, I explain why a consideration of legal disputes matters for scholars and practitioners interested in FDI. Then, I provide three sets of findings, from three distinct studies; the findings from the first two articles are more relevant for investors and government officials, as they deal with FDI political risk, while the findings from the third article are more relevant for a policy-oriented audience. I conclude with the overall policy implications of the research findings.

FDI Political Risk

Foreign investors operate across borders and are exposed to political risk, namely risk associated with factors under control of the host country’s government. Political risk may involve protection of property rights, constraints on the exercise of executive power, or respect for the rule of law. For example, in 2006, Bolivia nationalized its entire natural gas industry and Venezuela nationalized oil fields belonging to French and Italian firms. More recently, since 2020, there have been at least 18 investor–state disputes where the court ruled in favor of foreign investors, specifically citing unlawful expropriation by host countries (UNCTAD Investment Policy Hub).

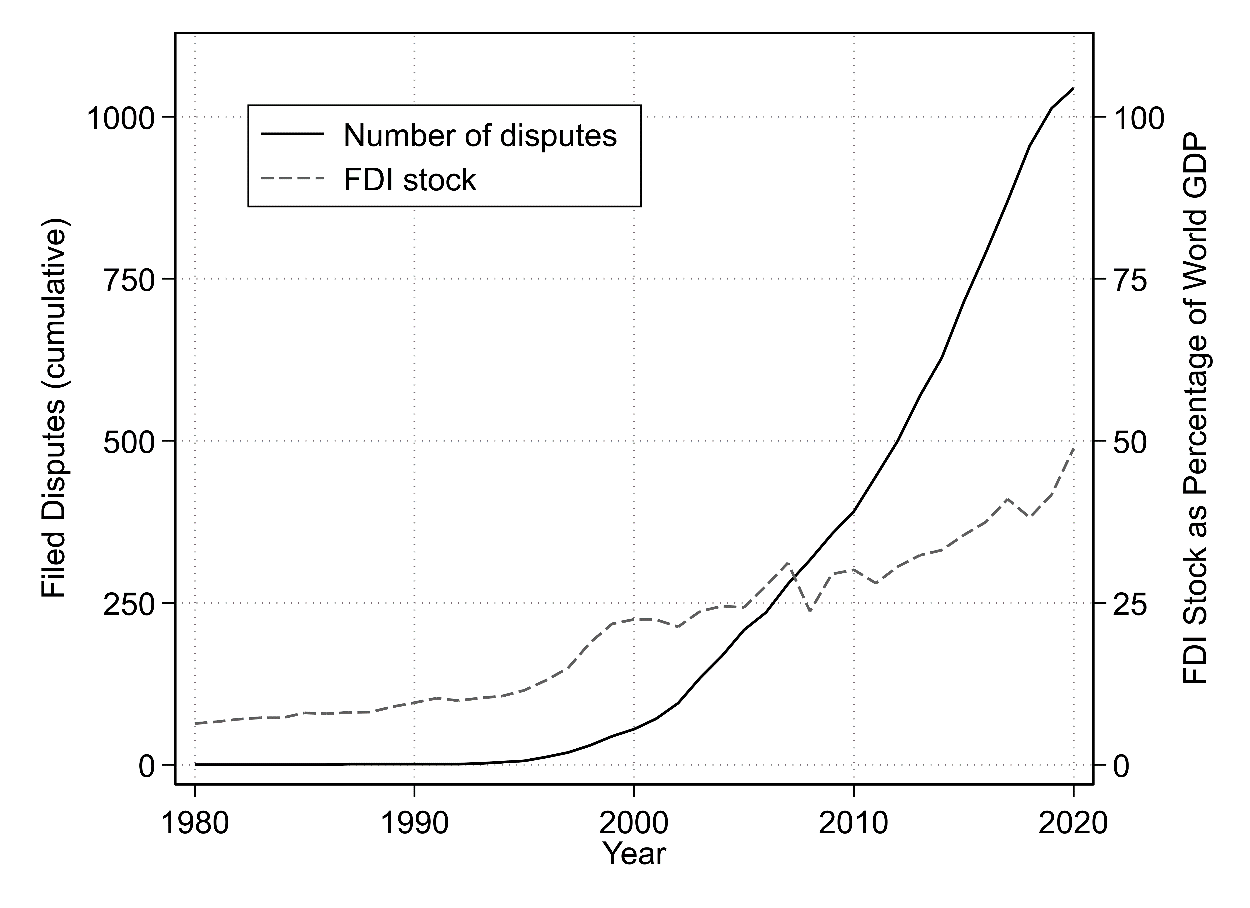

Between 1960 and 2014, more than 700 acts of government expropriation of FDI, by more than half the world’s countries, have been identified (Esberg & Perlman, 2023). Political risk is not new to foreign investment, but what makes the situation different today is the increasing reliance of MNEs on investor–state dispute settlement; the number of ISDS disputes has increased rapidly in the past two decades, so much so that there have been almost twice as many disputes in the past 10 years as ever before (Figure 1).

_stock_as_percentage_of_world_.png)

Evidence from Statistical Analyses

The first article examines the effects of international investment arbitrations on FDI flows. I built and analyzed a quantitative dataset including bilateral FDI flows and ISDS cases for all countries for which data were available; each data observation is uniquely identified by a directed dyad (home country to host country). I supplemented the ISDS cases made available by UNCTAD (Investment Policy Hub) with cases reported by other arbitral institutions (e.g. the International Court for the Settlement of Investment Disputes, or ICSID). I used multivariate regressions of FDI flows (dependent variable) on ISDS cases and outcomes (independent variables of interest), and include a series of political and economic control variables.

Finding 1: Based on recent data of ISDS cases and bilateral FDI flows, statistical evidence suggests new perspectives on reputational theories.

By “reputational theories”, I refer to international relations theories claiming that MNEs are less likely to invest in a country if that country was previously involved in investor–state disputes, because a history of disputes is taken as an indication the government is able and willing to breach contract or expropriate foreign investors (Allee & Peinhardt, 2011; Kerner & Pelc, 2022; Wellhausen, 2015). Some scholars have argued that the filing of even a single investment arbitration was enough to reduce FDI inflows (Aisbett, Busse, & Nunnenkamp, 2018).

However, from the newly-built dataset I find that:

-

Differently from what reputational theories suggest, filings alone seem insufficient to explain the relationship between ISDS and FDI flows. Since a dispute can have different outcomes (e.g. it can be won by the government, by the investors, or it can be settled), it is important to look at those outcomes.

-

Surprisingly, arbitration settlements can showcase host governments’ willingness to engage meaningfully with investors even after a filing. Conditional on a dispute’s having escalated to an international investment arbitration, a settlement is likely to happen only if the investors are satisfied by the government proposal.

If the aim is to assess causality between ISDS disputes and FDI flows, a caveat is that these findings are based on correlational evidence. To further understand the causal connection, it is necessary to unpack the links in the causal chain between ISDS disputes and FDI flows, together with their observable implications.

Evidence from Interviews

The second article assesses reputational theories of investor–state arbitrations and FDI. I used evidence from original interviews to assess specific and falsifiable hypotheses common to these theories.

Finding 2: Based on interviews conducted in Canada and Europe, I find that reputational theories would benefit from reframing.

To look more closely at the connection between disputes and FDI flows, I focused on two necessary causal steps of reputational theories. These steps are necessary because they are implicitly assumed in all of the field’s leading reputational theories:

-

MNEs are aware of investor–state disputes.

-

MNEs use information from investor–state disputes to make FDI investment decisions.

The assumptions mean that, if ISDS disputes are to be among the decisional factors in FDI locational decisions, then such disputes need to be known by MNEs, and MNEs should consider them relevant (see Figure 2).

_and_for.png)

To investigate the two assumptions, I interviewed 25 professionals in Europe and Canada who are connected with MNEs in different capacities, and who are involved in processes that influence or result in FDI decisions. This includes people in positions such as MNEs’ in-house counsels, international lawyers, national business leaders, managerial-level professionals working with international business networks and organizations, government officials, international civil servants, and experts involved in investor–state arbitrations as counsel or arbitrator. These interviews yielded several insights.

With respect to the first assumption, one respondent said “I would be very surprised if companies routinely followed cases in countries where they invest”. In fact, more than 70% of the interviewees said that they do not consider investor–state disputes relevant to MNEs; this group includes interviewees from MNEs, government officials, executives and managers at Chambers of Commerce and business networks, as well as FDI analysts. On the other hand, approximately one-quarter of interviewees, including international lawyers, said that there can be differences between large and small/medium companies with respect to tracking ISDS cases; only large MNEs are likely to devote resources and attention to tracking disputes. Overall, however, the interviews suggested that most MNEs do not track ISDS cases.

With respect to the second assumption, an in-house counsel for a MNE reflected that “we have never turned down a deal because of ISDS”. The counsel was very knowledgeable about ISDS cases and had accrued direct, hands-on experience in investment arbitrations. This and other statements strongly suggest that MNEs decisions do not rely on ISDS information, even when the company is aware of that information. Hence, the interview evidence suggests that some assumptions of FDI reputational theories need to be reframed.

Evidence from a Survey Experiment

The third article brings public opinion into the discussion and examines the trade-off between domestic policy autonomy and FDI attraction. To do so, I fielded a survey experiment in the United States to evaluate the factors that influence public preferences for government action in investor–state disputes.

Finding 3: The general public supports the government’s litigation (opposed to settlement) of disputes under certain conditions.

While FDI can have economic and political consequences for voters, beyond governments and investors, this study is the first to assess public support for government action on investor–state disputes, as far as I know. The study aligns with recent scholarship in political science that uses experimental methods to unpack intuitions about complex phenomena; for example, researchers found that public opinion influenced the foreign policy preferences of foreign policy leaders in the United Kingdom (Chu & Recchia, 2022). While conventional wisdom may suggest that FDI is a topic that is too complex for public opinion, scholars have found that citizens can be sophisticated consumers of information, and that investment arbitrations are usually covered by the media in the United States and elsewhere.

Furthermore, public opinion influences policy via selection, i.e., elections, and responsiveness, making it politically costly for incumbents to ignore public preferences (Tomz, Weeks, & Yarhi-Milo, 2020). The latter also applies in authoritarian environments (Fang, Li, & Liu, 2022).

I ran a survey experiment in the United States, on a nationally representative sample, to examine public support for government action in the face of an ISDS dispute. Survey participants were presented hypothetical scenarios of a foreign company suing their own government, with a randomized variation of five attributes regarding the relationship between the government, the foreign company and the foreign country. The five attributes pertained to economic aspects, such as the number of jobs created by the foreign company in the country, and political aspects, such as the regime of the partner country. When sued by a foreign company, a government can be more investor-friendly, and endeavor to settle the dispute, or less so, and continue litigating the case. The survey experiment tested which factors were more relevant for public support of one action or the other (settle or litigate). I found that the public is more likely to support litigation of a dispute if (i) there are past disputes from the MNE home country, or (ii) the political regime of the MNE home country is authoritarian. Other economic factors included in the experiment seem to have a lesser influence on public support, including concerns about job creation by foreign MNEs or the amount of total investment coming from the MNE home country.

Policy Implications

The dissertation’s different research strategies provide a powerful empirical combination that offers a comprehensive portrait of the reputational effects of international legal mechanisms on FDI flows. In particular:

- observational quantitative evidence speaks to broad patterns across space and time,

- interviews shed light on the operation of the theorized informational mechanism, and

- the survey experiment identifies individual-level effects.

The study sheds new light on:

-

Determinants of FDI, at a time when new industrial policies and FDI screening mechanisms are further promoting the securitization of trade and investment. While 17 countries had FDI screening mechanisms in 2014, 41 countries did by 2023 (UNCTAD, 2024).

-

Public support for investment treaties, at a time when developing countries are unilaterally rescinding their international investment agreements in the wake of public outcry ostensibly due to ISDS disputes (e.g., South Africa, India).

-

The role of transparency in government disputes, as it can have a measurable impact on public opinion and influence the (re)negotiations of investor rights and protections, at a time when about two-thirds of FDI stock in developing and least-developed countries is still under “old-generation agreements”, which offer broad investor protections that can clash with state regulatory autonomy, e.g. for environmental or social concerns (UNCTAD, 2024).

As mentioned, the conundrum for developing countries is often having to choose between greater domestic policy autonomy or FDI attraction. Given the potential beneficial effects and spillovers of FDI for developing contexts, and given that four out of five people today live in such economies, FDI can disproportionately impact the lives and livelihoods of the majority of the world’s population. Hence, it is crucial to improve our collective understanding of how FDI works, along with its consequences and determinants.

About the Author

Stefano Burzo earned his Ph.D. in Political Science from the University of British Columbia. His research primarily focuses on international political economy and quantitative methods. His dissertation studied the impact of international investment agreements on foreign investment using statistical analyses, interviews and a survey experiment. He also holds M.A. degrees from the University of British Columbia (in Political Science) and from the University of Florence (in Political Theory).