Introduction

When Jim Farley, CEO of Ford, returned from his 2023 trip to China, he knew the company was facing an “existential threat.”[1] Chinese electric vehicle (EV) manufacturers were pulling ahead rapidly, with a combination of low-cost production, advanced technology, and aggressive global expansion. Several Chinese EV models were shipped to Ford’s Michigan headquarters and tested by Ford’s executives and directors. This moment exemplifies how Chinese EMNEs are reshaping the competitive landscape not just in China, but globally.

This article introduces the concept of Global Value Chain (GVC) envelopment to explain how Chinese emerging market multinational enterprises (EMNEs) are outmaneuvering developed market multinational enterprises (DMNEs) like Ford in the global EV industry. GVC envelopment refers to the strategic process by which EMNEs enter and eventually dominate the global value chains of developed-market MNEs by leveraging partnerships with suppliers and integrating innovative capabilities. Drawing on the theory of platform envelopment (Eisenmann, Parker, & Van Alstyne, 2011), we argue that GVC envelopment involves EMNEs capitalizing on network effects and collaboration strategies to secure market share.

By examining the rise of Chinese EV firms such as BYD and CATL, we highlight how GVC envelopment is transforming industries and forcing incumbent players like Ford to rethink their strategies. This framework encourages international business scholars and practitioners to rethink global competition and understand how EMNEs use collaboration, innovation, and strategic partnerships to envelop established players within their own value chains.

Concept Development: GVC Envelopment

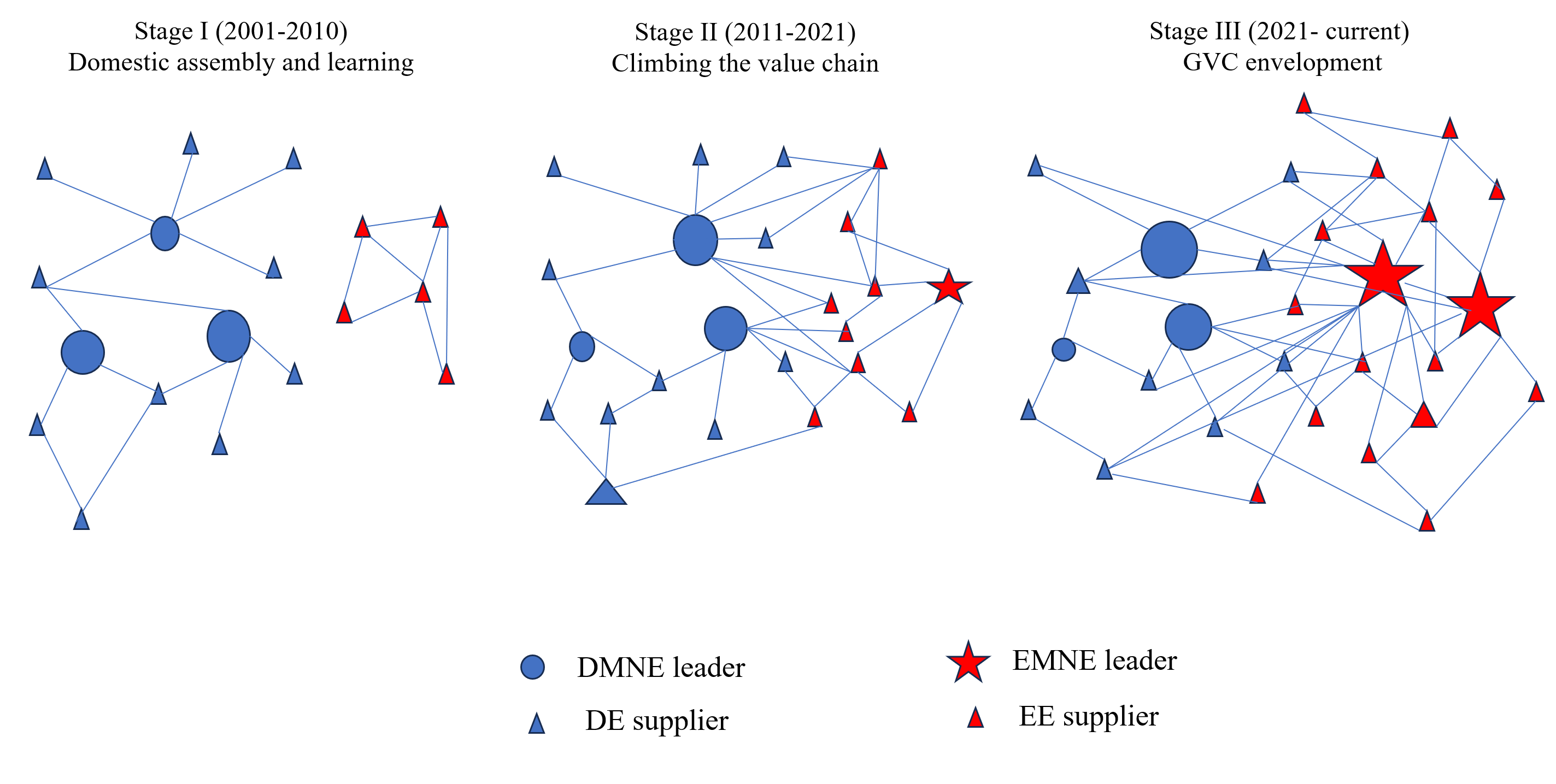

We develop a novel concept of GVC envelopment to explain how these EMNEs create synergies in GVCs and gain economies of scale, based on the concept of platform envelopment bundle (Allen, Chandrasekaran, & Gretz, 2021; Eisenmann, Parker, & Van Alstyne, 2011). GVC envelopment refers to the strategic process where one multinational enterprise (usually an EMNE) expands into another multinational enterprise’s (usually a DMNE) GVC, by forming cooperative relationships with the target’s suppliers and partners within the value chain network. The goal is to leverage these combined resources to capture market share from the DMNE, effectively enveloping its role in the value chain. Similar to the concept of platform envelopment, GVC envelopment emphasizes that an EMNEs is able to extend its business activities by integrating or incorporating the functionalities of a related DMNE to capture its user base and expand its market presence via leveraging existing assets, customer relationships, and capabilities. While the theory of platform envelopment (Allen et al., 2021; Eisenmann et al., 2011) assumes that network effects, multi-sidedness, and modularity are critical characteristics in platform-based competition, similarly, we argue that GVC development shares the similar characteristics, especially in innovation and competition in emerging industries like the EV industry (Eisenmann et al., 2011). In our analysis of the EV industry in China, GVC envelopment manifests as EMNEs (e.g., Chinese automakers) integrate themselves into the GVCs traditionally dominated by DMNEs, not only by partnering with key suppliers but also by incorporating technological and market innovations that enable them to capture significant market share. Hereby we explain the three-stage evolution below to illustrate the process of GVC envelopment. Figure 1 shows the evolution process.

Stage I (2001-2010): Domestic assembly and learning: China joined the World Trade Organization in 2001 and implemented a series of reforms and new policies to open up the auto market and promote the development of domestic auto value chains. DMNEs like Volkswagen, General Motors, and Toyota dominated China’s market. Domestic suppliers entered the GVC via forming joint ventures with and receiving technology transfer from foreign automakers, primarily concentrating on assembly and low-value-added activities (Harwit, 2001).

Stage II (2011-2020): Climbing the value chain: The Chinese domestic suppliers experienced rapid growth and diversification, and some EMNEs emerged and gained significant market share, e.g., Chery, Geely, and BYD. Both DMNEs and EMNEs increased inward sourcing (Zhou, Yan, & Sun, 2022) and collaborated with the domestical suppliers in component production and subassemblies . For example, after building its Gigafactory in Shanghai, Tesla developed over 400 local first-tier suppliers in China, of which more than 60 suppliers have entered Tesla’s global supplier list. The inward sourcing or localization rate of Tesla in China has exceeded 95% for all components.[2]

Stage III (2021- current): GVC envelopment: EMNEs started to lead the GVC through advancements in electrification, autonomous driving, and other digital technologies. They are transiting China’s auto industry from mostly traditional gasoline-powered vehicles to EVs, and expanding into international markets rapidly, even in developed countries. For example, BYD overtook Tesla in global EV sales in the last quarter of 2023 and has planned to build factories in Hungary and Mexico.[3] In this stage, EMNEs could advance these tactics for GVC envelopment as the surrounding forces converge:

-

GVC penetration: EMNEs enter the existing GVC currently controlled by the DMNEs in securing access to raw materials or establishing their own vertical production of key components.

-

GVC integration: EMNEs closely collaborate and share knowledge with suppliers, which are deeply embedded in DMNE’s network.

-

GVC co-evolution: EMNEs co-evolve with DMNE lead firms (Lema, Pietrobelli, & Rabellotti, 2019; Lema, Rabellotti, & Gehl Sampath, 2018). This suggests a more dynamic and mutually beneficial relationship between the two lead firms. Establishing their own distribution channels or brand recognition to bypass the DMNE’s dominance in the final product market.

The Characteristics of GVC Envelopment

Treating GVCs as asymmetrical networks, Kano (2018) emphasizes the orchestrating role of the lead firm in GVCs and proposes social mechanisms facilitating coordination and fostering innovation. We use this discussion and provide a comparison of GVCs led by DMNEs and EMNEs in Table 1. This comparison and Kano’s (2018) assumption of GVCs as asymmetric low density/high centrality networks, allows us to characterize GVC envelopment.

Our concept of GVC envelopment emphasizes network dynamics and instability– an EMNE could challenge the centrality position of a DMNE; lead/orchestrate the green innovation path of GVCs; generate new relational capital in GVCs; improve GVC efficiency, especially in the global green transition. Therefore, GVC envelopment could manifest a new governance form in GVCs, drift power dependence, and change value creation/distribution. We suggest these characteristics of GVC envelopment in a lower-centrality network of a GVC:

-

EMNEs as new orchestrating firms in GVCs. EMNEs that compete on green products (e.g., EV manufacturers) develop disruptive business models with new products within GVCs, promoting resource efficiency and circularity by adopting innovative eco-friendly technologies (Ito, Ikeuchi, Criscuolo, Timmis, & Bergeaud, 2023). The disruptive business models that EMNEs have adopted help them share knowledge and expertise with smaller GVC participants (suppliers) in emerging economies than DMNEs, to help smaller GVC participants adopt sustainable practices and improve their environmental performance, finally improving GVC efficiency and delivering affordable products (Qin & Sun, 2023).

-

Suppliers with low power dependence on DMNEs. There are high power asymmetries between lead firms (usually DMNEs) and suppliers in GVCs (Gereffi, Humphrey, & Sturgeon, 2005; Lema et al., 2019; Lema, Quadros, & Schmitz, 2015; Strange & Humphrey, 2019). In Stage I, Chinese suppliers are highly dependent on DMNEs for technology transfer and knowledge production process; however, they are catching up fast. For example, CATL started manufacturing lithium-polymer batteries for consumer electronics in 1999, secured early partnerships with domestic automakers like BAIC and Geely in 2012, and surpassed Panasonic to become the world’s 3rd largest EV battery supplier in 2016. CATL has collaborated with several major automakers to develop and supply batteries for EVs, including BMW, Teslaa and Ford. Suppliers from emerging economies could gain power in GVCs through knowledge acquisition, relationship learning, and collaboration (Herrigel, Wittke, & Voskamp, 2013; Jean, Kim, & Sinkovics, 2012; Qin & Sun, 2022). A unique context of China is that the growth of innovative domestic suppliers with low power dependence on DMNEs contribute to the success of Chinese lead firms in GVCs, via knowledge sharing and collaboration and providing high-quality components (Zhou et al., 2022).

-

Scale and speed in GVCs. In Stage II and Stage III, both lead EMNEs and Chinese suppliers strengthen manufacturing and production capacity. This capacity allows Chinese EMNEs to mass-produce green products, such as solar panels, wind turbines, and EVs, potentially driving down costs and making these technologies more accessible to the global audience. This shows that scale and speed are two crucial aspects of manufacturing capacity in GVCs. Their interplay shapes efficiency, competitiveness, and overall resilience of these interconnected production networks (Lee, Kim, Choi, & Jiménez, 2023; Morris, Oldroyd, Allen, Chng, & Han, 2023).

-

Distributed innovation systems. When more geographically dispersed players, including lead EMNEs, lead DMNEs, suppliers from emerging economies and developed economies, collaborate, co-create, and add more modularity and interconnections in GVCs, this loose-coupled system becomes a distributed innovation system, with more knowledge exchange, interconnectedness, and open innovation (Fischer, Meissner, Boschma, & Vonortas, 2024; Nambisan & Luo, 2021). Chinese domestic suppliers are collaborating actively with EV manufacturers in the areas of energy storage technology and battery management system (Zeng, Li, & Liu, 2015). Lead EMNEs could encourage decentralized problem-solving and facilitate the exchange of green innovation ideas among participants other than suppliers. For example, in a comparison of patent applications, Nikkei editor found that the Chinese EV powerhouse BYD has filed an impressive 16 times more patents than its counterpart Tesla. BYD strategically employs legal frameworks to safeguard its battery technology, while Tesla leans heavily on production advancements.[4] Finally, GVC envelopment leads to an inclusive innovation ecosystem which involves all GVC players in the innovation process and makes GVCs more resilient and sustainable.

Conclusion

In this paper, we introduced the concept of GVC envelopment to explain how EMNEs, particularly in green industries like EVs, are innovating and competing with DMNEs. As Ford’s experience shows, the rapid technological and market progress of Chinese firms, combined with their deep integration into local and global supply chains, presents a serious challenge to incumbents.

We propose a three-stage development of GVC envelopment. EMNEs usually start by collaborating with lead DMNEs and gradually take on market share that lead DMNEs are unwilling or unable to capture to move up along the value chain (Zhou et al., 2022). In this stage, EMNEs leverage innovation resources within the GVCs initiated by lead DMNEs by utilizing their unique learning and innovation capabilities, and build their own supply relationships and network to form a multi-value chain bundle, finally enveloping the existing stakeholder relationships inside the GVC and replacing lead DMNEs. Through envelopment, EMNEs can leverage the GVC’s existing knowledge, resources, and relationships to gain an advantage over the incumbent DMNEs. EMNEs can also exploit innovations and opportunities in the target GVCs, and offer better or cheaper products to global customers. Incumbent DMNEs may be unable to respond effectively, as they focus on traditional value chain activities, and may lose market share, profitability, and reputation in the end.

Our concept further highlights the importance of resource linkage, leverage and learning in the internationalization process of EMNEs (Mathews, 2006). The envelopment strategy is not static; it evolves over time. In the global green transition, it began with learning and positioning, transitioned into encircling and challenging the dominant players, and now culminates in a full-scale assault on the GVC. By understanding this dynamic and evolving process where EMNEs leverage collaboration and innovation to envelop established players, scholars and practitioners can better anticipate shifts in global value chains. This framework pushes IB research to consider not just competition, but also the nuanced ways in which EMNEs can integrate themselves into—and eventually dominate—global GVC, particularly in sectors undergoing rapid technological and green transitions.

This research provides important managerial implications. For EMNE managers, it shows the importance of local supply chain upgrading. By adopting innovative practices and leveraging resources in GVC, EMNEs can enhance efficiency and competitiveness of their domestic operations. Additionally, strengthening international collaborations allows EMNEs to pool resources, access advanced technologies, and gain market insights. This approach not only optimizes the use of global resource advantages but also positions firms strategically in the global market, enhancing their capacity to address complex challenges. For policymakers, this research shows that by providing financial incentives, tax benefits, and R&D grants, policy making can accelerate the adoption of sustainable practices in GVCs. Furthermore, fostering knowledge-sharing platforms and enhancing industrial infrastructure will create a conducive environment for sustainable innovation. These efforts collectively ensure a more robust, sustainable, and inclusive industrial ecosystem, helping EMNEs to compete effectively while contributing to broader sustainable development goals.

Acknowledgement

Sun acknowledges the financial support from the National Natural Science Foundation of China (Grant ID 72232010, 72091311, and 72172154).

About the Authors

Sunny Li Sun is an associate professor of entrepreneurship and innovation at the University of Massachusetts Lowell and Alan Rugman Fellow in University of Reading. His research interests cover entrepreneurship, corporate governance, venture capital, network, and institutions. He is a Boston-qualified marathon runner.

William C. Zhou is an assistant professor of management at Welch College of Business & Technology, Sacred Heart University. His research interests include innovation, sustainability, and DEI policy.

Colias, M. (2024) What Scared Ford’s CEO in China, Wall Street Journal, Sept. 14. https://www.wsj.com/business/autos/ford-china-ev-competition-farley-ceo-50ded461

Ma, Si. (2023) Tesla grows together with local suppliers, Nov. 29, China Daily, https://cn.chinadaily.com.cn/a/202311/29/WS656706bba310d5acd8770ed0.html

Toh, M. (2023) Mexico could help this huge Chinese carmaker crack the US market, Jan. 19, CNN. https://www.cnn.com/2024/01/19/cars/byd-hungary-mexico-global-domination-intl-hnk/index.html.

Shimizu, M. (2023) BYD outpaces Tesla 16-fold in patent filings. Nikkei Asis. Sept. 21. https://asia.nikkei.com/Spotlight/Electric-cars-in-China/BYD-outpaces-Tesla-16-fold-in-patent-filings.