Introduction

Emerging market multinational corporations’ (EMNE) strategic choices are driven by the characteristics of their home institutions and the constant evolution of these environments (Peng, Wang, & Jiang, 2008). Researchers have focussed on their aggressive catch-up behaviour through outward foreign direct investment (OFDI) (Luo & Tung, 2007). Faced with enhanced competition locally and globally, OFDI helps them acquire capabilities and compete globally. While home institutional transformation has spurred them on, the evolving corporate governance (CG) environment has also been instrumental in shaping their responses.

Intuitional voids, a weak regulatory system and consequent high transaction costs create market imperfections (Khanna & Palepu, 2000). Not only is the environment deficient for capability upgradation, but it also renders the mechanisms for aligning the principal–agent interest (arm’s-length agency contracts) ineffective (North, 1990). The national institutional structure also impacts the bundle of internal and external governance mechanisms (Young, Peng, Ahlstrom, Bruton, & Jiang, 2008). With these prevalent institutional characteristics, how firms make strategic decisions and what hinders or facilitates them can have important managerial implications.

Given the institutional complexities, certain organisational forms and ownership structures have evolved, creating unique agency issues. Organisational forms such as state-owned enterprises (SOEs) (Zhu, Tse, & Li, 2019), family firms (FFs) and business groups (BGs), with concentrated ownership (Holmes, Hoskisson, Kim, Wan, & Holcomb, 2018), have emerged to fill the voids of resources, trust and norms of acceptable behaviour (Bhaumik, Driffield, & Pal, 2010). However, these firms’ decision-making is frequently dominated by large controlling shareholders (often multiple generations of a family), resulting in numerous principal–principal conflicts (Young et al., 2008). Such family-owned/controlled businesses (FFs) are primarily in emerging markets (EMs) (Karaevli & Yurtoglu, 2021). For example, India and China have a large number of publicly listed FFs. Succession planning and lack of transparency in practices are key governance concerns hampering growth, in addition to rapid technological disruptions (PWC, 2023).

FFs, BGs and SOEs are now at the forefront of EM firms evolving into EMNEs (Wang, Hong, Kafouros, & Wright, 2012). Valuable lessons from foreign alliances helped BGs such as TATA and Mahindra while expanding abroad. Infosys, a similar exemplar, adopted global CG standards and listed on globally benchmarked bourses, despite having no requirement for foreign capital (Khanna & Palepu, 2004). Their global growth and reputation are attributed to these bold moves that they took prior to their success abroad, rather than being a result of it (Khanna & Palepu, 2004). Such reputation signalling aided their global acquisitions later.

However, concentrated ownership, a key feature of EM firms, continues to hinder the effectiveness of some CG mechanisms that are popular in developed markets. Mechanisms like the market for corporate control and oversight by independent directors, which are popular in developed markets for promoting transparency in corporate actions, continue to be overshadowed in EMs. For example, the ineffectiveness of proxy advisory firms could be seen in the Board’s appointment of Mukesh Ambani’s youngest son despite their advice against it (Business Standard, 2023), while the long tenures enjoyed by independent directors in the now collapsed firms Evergrande and Country Garden in China puts the spotlight on CG lapses (South China Morning Post, 2024).

Hence, while such organisational forms fill certain institutional voids, they can also be counterproductive. Owners at FFs, who are often seen as controlling owners, may seek rents at the expense of other shareholders. They may even restrict operations, despite potential growth opportunities, to preserve their family identity and control (due to social emotional wealth, SEW) (Gómez-Mejía, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007). However, recent reports on Indian FFs (PWC, 2023) suggest that more than two-thirds of them desired new market entry. Further, more than 71% of them experienced growth in their global operations (PWC, 2023). Table 1 and Table 2 depict the OFDI from India and the changing ownership patterns of NSE-listed firms between 2007 to 2023. Despite dips, the consistent recovery of OFDI coincides with a high promoter holding, averaging 30% over the period (Table 1), but a decline in Government ownership. Foreign institutional investors (FIIs) continue to play a significant role with an average of 19.4 % ownership across firms (Table 2). Though concentrated ownership persists, the rise of institutional ownership, especially domestic mutual funds and FIIs (Table 2, 3), has had a positive effect on OFDI. Table 3 compares the rising mutual funds and FIIs holdings of a subset of NSE-listed firms (for 2011, 2015 and 2023) and their OFDI (marked in green in Table 3). However, the role of FIIs in OFDI decisions remains muted in state-owned firms. (e.g., Bharat petroleum in Table 3.) Compared to 2011, ownership by banks and financial institutions has declined (decline marked in red in Table 3).

Hence, there is a need to reconcile the unique characteristics, the changing patterns of their ownership structures and organisational forms, and the mechanisms that enable them to venture abroad. Given the complexities of OFDI decisions, how do EMNE managers deal with the CG issues emanating from their unique ownership and organisational structure? How do they achieve their global objectives? The following sections bring together extant literature on this issue and distil ideas that would help managerial responses.

Characteristics of EMNEs: Ownership Structures

Two distinct characteristics of EMNEs, concentrated ownership and FFs/BGs, create unique governance challenges across EMs.

Controlling Owners

The governance of firms in developed markets overcomes principal–agent conflict owing to dispersed ownership of principals, as well as governance structure of aligning agents’ interests with principal interests using incentive mechanisms. Hence, governance needs to align the interests of agents (viz., managers) with those of dispersed owners (principals). In EMs, one of the principals is also the agent (or controlling owners). This forms the root of principal–principal conflicts in EMs (Young et al., 2008). Controlling owners significantly influence firm expansion. Family owners, BGs and the state have controlling rights in EM firms (Hu & Cui, 2014) and impact firms’ propensity to invest (Bhaumik et al., 2010).

Diversified family-owned BGs connect semi-autonomous firms through ownership, business relationships, director interlocks and/or social ties (Holmes et al., 2018). BGs allow firms to overcome capital market imperfections and fill gaps product and labour markets (Khanna & Palepu, 2000). BG affiliates benefit from the overseas experience of fellow affiliates(Elango & Pattnaik, 2011), which informs their location and entry mode choices (Holmes et al., 2018). It also helps them act early during merger waves (Popli & Sinha, 2014). Their access to group capital and risk sharing (Holmes et al., 2018) makes them less dependent on FIIs than stand-alone firms when investing abroad (Chittoor, Aulakh, & Ray, 2015). BGs in general and larger, less diversified firms tend to have greater OFDI (Chari, 2013). While they provide resources, BGs can paradoxically foster opportunism. This is exacerbated in EMs due to pyramidical ownership (complex, layered ownership), principal–principal conflicts and dual controls by affiliates’ own and group-level management (Holmes et al., 2018).

Likewise, family-controlled firms can play either a facilitative role (stewardship, alignment of family and business goals) or a restrictive role (preserving SEW and hence refraining from risky OFDI) (Karaevli & Yurtoglu, 2021). The unification of ownership and control under a single executive from the family further inhibits OFDI. FFs often avoid OFDI, even if it means below-target performance (Gómez-Mejía et al., 2007). Additionally, non-family managers’ involvement in such decisions is undermined when key decision-making positions are reserved for family members (Kerai, Kumar, & Singla, 2023).

SOEs, with the state as dominant owners, are part of the institutional set-up and are guided by political affiliation (Cui & Jiang, 2012). Hence, their motives/modes of international entry are guided by state agendas, namely resource-seeking, technology and capability upgradation in the home country (Hu & Cui, 2014; Wang et al., 2012). However, high state ownership can hinder technology-seeking in developed markets, as host nations may perceive these firms as politically motivated (Cui & Jiang, 2012; Wang et al., 2012).

While some studies show that despite their resource provisioning role, SOEs discourage OFDI (Hu & Cui, 2014; Panicker, Upadhyayula, & Sivakumar, 2022), others show their positive impact in certain sectors and for specific motives. For example, Chinese SOEs invest in resource-rich and politically risky locations (Ramasamy, Yeung, & Laforet, 2012). This reinforces their aggressive entry, driven by resource requirements at home (Cui & Jiang, 2012). Higher levels of Government affiliation and ownership impose their agenda more as EMNEs invest abroad (Wang et al., 2012). Government involvement in Chinese firms has created ‘corporate empires’ (economically unjustifiable firm growth) (Zhu et al., 2019) with distinct agency issues. Such SOEs, through foreign capital, can curtail empire building and build a reputation prior to international investments (Zhu et al., 2019).

Non-Controlling Owners

Shareholding types differ across national laws, with some categories dominating based on the development of national institutions. The management, employees, foreign investors and lenders comprise non-controlling owners with minority shareholding. Financial partners are key stakeholders for FFs. Securing their trust is as important as that of consumers and employees (PWC, 2023) .

“Important” non-controlling shareholders, such as domestic institutional investors (DIIs) and foreign corporates (FCs), provide tangible (finances) and intangible resources (foreign market knowledge) facilitating OFDI (Hu & Cui, 2014). Non-controlling owners are important as FFs may need external finances and may need to signal good internal governance (for example, by appointing independent directors to the board) (Bhaumik, Driffield, Gaur, Mickiewicz, & Vaaler, 2019). Hence, hybrid ownership of state or FFs with institutional investors (IIs) is common in EMs.

IIs (domestic/foreign), such as banks, mutual funds and pension funds, differ from family owners in their risk preferences. Hence, they moderate the negative impact of family ownership on OFDI. The impact of the presence of IIs in EMs differs from that in developed markets due to the unique principal–principal problem (Young et al., 2008). However, different categories of IIs vary in their risk perceptions as well as the risk propensity consequently impacting their strategic decisions (Panicker, Mitra, & Upadhyayula, 2019).

Among them, FIIs foster managerial ability for internationalisation decisions and are valued for their global experience and knowledge (Chittoor et al., 2015). Their familiarity with international markets facilitates OFDI.

Domestic Institutional Investors (DIIs) comprise banks, financial companies, insurance companies, mutual funds (MFs), and pension funds. Lenders on the board act against OFDI, due to their combined debt and equity stakes (Panicker, Upadhyayula, & Mitra, 2023). As nominee directors in FFs, their focus is on a firm’s ability to repay loans (Panicker et al., 2019). DIIs perceive international investments as a potential hinderance to debt recovery (Panicker et al., 2019, 2023). In contrast, DIIs enjoy a multifaceted relationship with the SOEs as investors, lenders and advisors, thereby facilitating higher investments (Panicker et al., 2022). However, Chinese SOEs must curtail managerial empire building through long-term debt (Zhu et al., 2019).

Other categories of non-controlling shareholders, like employees and individuals, have limited voting rights and little influence on strategic decisions. In fact, dispersion of ownership to risk-averse minority shareholders and to later generations in the same family discourages internationalisation (Karaevli & Yurtoglu, 2021). Hence, EMNCs need to choose which categories of shareholders to divest to, in order to promote OFDI.

Characteristics of EMNEs: Upper Echelons

TMT and Board Characteristics

Beyond ownership structures, the governance efficacy and ability to handle enhanced complexities of OFDI also depend on top-management characteristics like CEO compensation, TMT composition and board structure (Hu & Cui, 2014; Sanders & Carpenter, 1998). A powerful CEO can escalate principal–principal conflicts (Hu & Cui, 2014). The positive influence of resources provided by non-controlling investors on OFDI may be weakened under self-seeking powerful CEOs (Hu & Cui, 2014). Even long-term debt, a monitoring mechanism in advanced markets, becomes an instrument for empire building in SOEs (Zhu et al., 2019).

In EMs, the board functions more as advisors and resource providers (Singh & Delios, 2017). Their capacity to oversee self-serving management is frequently insufficient. Hence, concentrated ownership and opportunistic behaviour elevate the importance of external board characteristics in EMs. Industry-specific and international experience of independent directors(Chittoor et al., 2015), interlocking directorate (Edacherian & Panicker, 2022), and network centrality (Singh & Delios, 2017) enhance EMNE resources. While inside director interlocks positively influence exploitative OFDI, independent directors tend to discourage it (Edacherian & Panicker, 2022). CEO duality, which is rarely seen in developed markets, helps facilitate OFDI decisions of EMNEs by offering ‘unified authority’ (Singh & Delios, 2017).

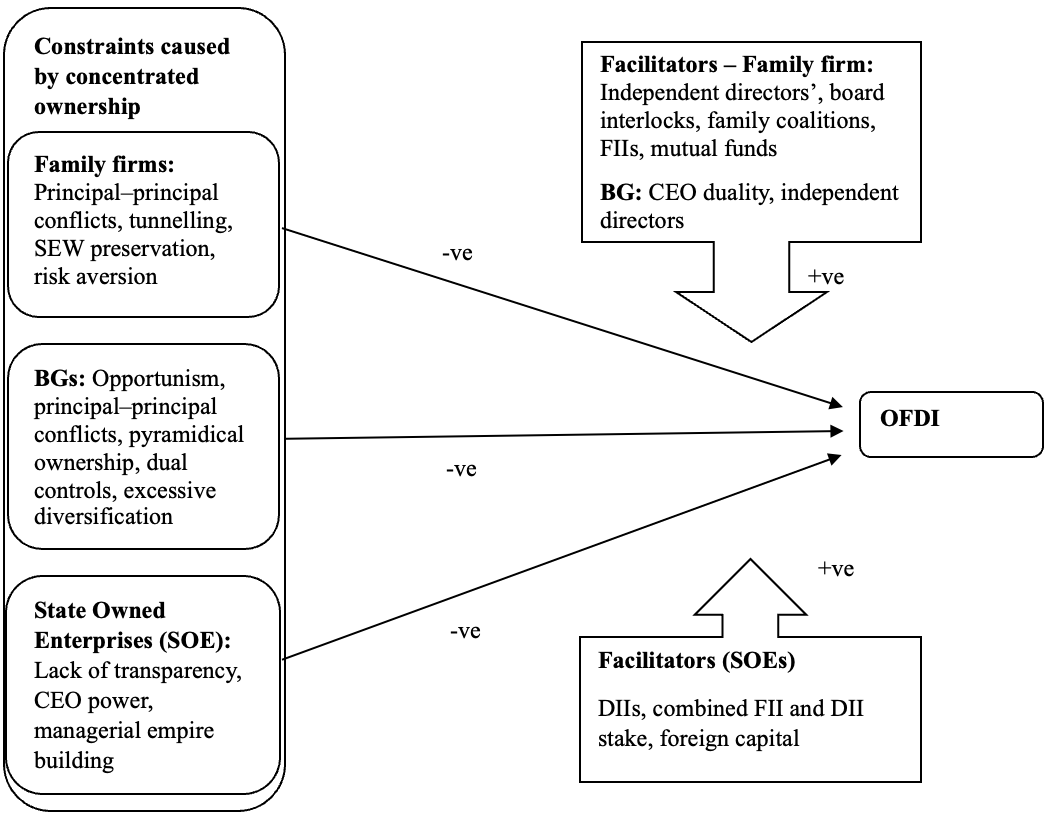

Figure 1 summarises the themes, the main CG mechanisms in EMs, and the constraints and facilitators of OFDI for EMNEs. It synthesises the extant findings with different implications based on the firm’s ownership structures.

Insights for Owners/Managers

CG issues unique to EMs “alter dynamics of the CG process” (Young et al., 2008). Conventional agency solutions like the independence of the board, market for corporate control and managerial equity alignment are hence ineffective in markets with institutional voids (Zhu et al., 2019). The solutions highlighted in extant studies for managers and owners in EMNEs are listed below:

-

Ownership structure in EMs is dependent on the nature of decisions of the controlling owners.

a. FFs are seen to involve IIs to overcome risk aversion and add to their managerial capability. FIIs and MFs, with their low-risk perception of FFs and their inherent ability to take up higher risk, facilitate OFDI. FFs need to rely more on FIIs and MFs and reduce their dependence on debt. FIIs mandate better internal governance and better reporting among FFs, enabling them to gain legitimacy in foreign markets (Panicker et al., 2019).

b. SOEs could raise financial resources through the transfer of ownership to DIIs. However, FIIs’ influence on OFDI in SOEs is subdued by state interference (Panicker et al., 2022). Chinese SOEs affiliated to higher levels (Provincial/National) of the Government are driven by normative pressures to achieve higher competitiveness and capability upgradation and hence invest in advanced economies (Wang et al., 2012). Resource limitations that hinder OFDI by SOEs can be resolved through hybrid ownership formats. Hybrid ownership of firms, by the state and IIs, provides valuable resources to SOEs (Panicker et al., 2022).

c. High diversification at BGs and dual controls (group and affiliate level) may hinder OFDI. The unified authority of the same person serving as CEO and board chair can reduce conflicts of interest. Also, independent board members, through their interlocks, can also help firms pursue international growth.

d. Multi-family coalitions have also facilitated OFDI in Turkish firms. Such coalitions strengthen internal governance, facilitate risk sharing and enable mutual monitoring (Karaevli & Yurtoglu, 2021). Their combined knowledge and experience mitigate risks, restrict opportunism and alleviate uncertainties in internationalisation (Karaevli & Yurtoglu, 2021). Among FFs, a higher promoter stake encourages risk taking and increases OFDI (Chittoor et al., 2015; Singh & Gaur, 2013). Therefore, ownership by specific categories of shareholders aids OFDI.

-

The adverse effects of structural power concentration on OFDI can be mitigated by giving some key decision-making positions to non-family members (Kerai et al., 2023). This is necessitated in highly competitive industries where risk aversion by family members and SEW preservation goals can hamper growth (Kerai et al., 2023).

-

Strategic investments by foreign corporations (FC) can negate the opportunism among powerful CEOs in EMNEs. Unlike the tangible contributions from DIIs, the intangible and knowledge-based benefits gained from FCs cannot be opportunistically appropriated. Rather, their presence encourages CEOs to build their reputation by supporting internationalisation (Hu & Cui, 2014). Thus, boosting CEO power through enhanced compensation can result in desired OFDI outcomes and nurture strategic partnership with FCs. CEOs’ duality offers unified authority, which facilitates OFDI. It is also supported by CEOs with foreign experience (Chittoor et al., 2015; Singh & Gaur, 2013)

-

Firms in China, desirous of OFDI must onboard Govt agents at the state or provincial level rather than at the city or county level (Wang, Hong, Kafouros, & Wright, 2012).

Conclusion

In this article, we highlight some EM-specific CG practices and their implications for the OFDI decisions of EMNEs. OFDI is a key strategy for EM firms’ growth as they face enhanced competition at home and abroad. The differences highlighted in investor preferences observed in China, India and Turkey point to the importance of contextualising CG issues based on the firm’s institutional environment. EM firms need to address CG barriers to international investment. Actions like coalition-family ownership, increasing the stake by FIIs and mutual funds in FFs, strategic investments by FCs in listed firms, support foreign investments through knowledge and resources. While among Indian listed private firms, limiting the creditor-investor’s role can facilitate OFDI, FII and DIIs together boost OFDI decisions in Indian SOEs. Hence, managers need to make firms more attractive to FIIs. Pursuit of OFDI is emerging as a safeguard against the usual governance lapses characteristic of EMNEs.

About the Authors

Rajesh Srinivas Upadhyayula is a professor of Strategy at the Indian Institute of Management, Kozhikode, India. He is an experienced faculty with a demonstrated history of working in the higher education industry, in the areas of Internationalisation, Platform ecosystems, Corporate Governance, Entrepreneurship. He has published in leading journals like the Journal of World Business, Journal of international Management, Journal of Business Research.

Tina Thomas is a doctoral student, in Strategy at the Indian Institute of Management, Kozhikode, India. Her doctoral thesis advisor is Prof. Rajesh Srinivas Upadhyayula. Her research interests include Emerging Market Multinationals and their strategic decisions.