African multinational enterprises (MNEs) – like any other MNE – occasionally need short-term working capital and long-term project finance in a foreign currency, for example to pay foreign suppliers or support ventures into new (typical other African) countries. Yet many African countries do not have a reliable stock of foreign reserves to support such transactions. For example, for an underdeveloped, oil-dependent economy like Nigeria or Angola, a lower oil price can dramatically affect foreign reserves. Moreover, African governments often run out of foreign currency because they try to “protect” the value of their currency (Sanusi, Meyer, & Hassan, 2019).

This poses a particular challenge to Africa-based “nascent MNEs”. Nascent MNEs are small MNEs from lower income home countries that operate primarily in other lower income countries (Ibeh, Adeleye, & Ajai, 2018). Suffering from the liability of smallness (Acheampong & Rand, 2023) and lacking a parent in a middle- or high-income country (Barnard & Mamabolo, 2022), nascent MNEs are especially vulnerable to the institutional dysfunction of the African environment. How do the managers of such nascent MNEs deal with African capital market voids?

The use of political connections is one of the most frequently mentioned strategies (Wang, Cui, Vu, & Feng, 2022; White, Hemphill, Rajwani, & Boddewyn, 2020) to overcome institutional voids (Khanna & Palepu, 2010). But capital market voids differ in an important way from voids in labor or product markets: If there are not enough foreign reserves, governments must ration capital. Under those conditions, even political connections may not get MNEs enough foreign funds for their needs.

In making sense of how African managers seek funding, the Latin American experience is useful. Chu (2021) underlines the importance of institutional quality and a sound macro-economic environment in supporting access to finance in Latin America, while also confirming that larger and older firms find financial access relatively easier. Still, underdeveloped capital markets in Latin America predispose even large firms to rely heavily on debt (Díaz-Rivera, 2024). However, banks often “retreat from financing small and medium-sized enterprises” (Godke Veiga & McCahery, 2019: 633), with private equity and venture capital funds suggested as alternative sources of funds.

Given that much of Africa is characterized by similar economic turbulence, underdeveloped capital markets and dysfunctional institutions (Barnard, Amaeshi, & Vaaler, 2023), it is likely that access to finance in Africa will be as – if not more – complex and cumbersome as in the case of Latin America. We wanted to understand the types of finance that executives working in Africa sought, what the process entailed, and what obstacles they encountered.

Methodology

To gather data, we polled finance executives of an African MNE with a footprint across sub-Saharan Africa. Funding for its subsidiaries is decentralized, and arranged by the finance executives in the different countries of operation, with the parent providing guidance on funding structures and security arrangements. These executives therefore had first-hand knowledge about seeking capital in their respective counties, specifically Botswana, Kenya, Malawi, Mozambique, Tanzania, Zambia and Zimbabwe.

Table 1 provides contextual information about the countries. They are mainly low-income or lower-middle income countries, with only Botswana achieving upper middle-income status. Net FDI inflows are typically well under US$ 1 billion per country per year. (Outward FDI was negligible and ranged between 0% and 0,8% – for Mozambique – of GDP.) In terms of governance indicators, Botswana ranks among the top third in the world, but all the other countries tend to be in the bottom third, with Zimbabwe close to the bottom decile.

Interviewing the seven MNE executives provided useful and granular insights, but as with any single case, questions can be raised about the wider applicability of their experiences. To make sure that we were capturing general challenges in the African environment, we also conducted interviews with nine finance intermediaries who worked in the region, particularly from commercial banks and development finance institutions. These intermediaries were located in Botswana, Kenya, Malawi, Mozambique, South Africa, Zambia and Zimbabwe. We asked them to reflect on firms’ experiences in Africa more generally, and specifically the time it typically took to obtain various types of capital, the terms and interest rates available, and to explain why. Their estimates and explanations were consistent with the information provided by the executives. Data gathering took place from August to October 2024.

Very Basic Funding Sources Functioning Quite Inefficiently

As one of the managers of a commercial bank mentioned, Africa-based executives typically looked for “vanilla-type products”, with low demand for “more structured and creative” forms of financing. Indeed, the executives to whom we spoke mentioned vehicles like overdrafts, short-term loans and revolving credit facilities. The supporting instruments through which they were offered were typically letters of credit, bank guarantees, invoice discounting and debt factoring. These instruments were used to obtain capital both in the local and in foreign currency. Even these quite basic instruments often did not operate particularly efficiently. One executive explained the process:

So the whole process would now start with the supplier giving us a pro forma or an invoice which we then need to submit to our clearing agent, who then raises this terms and conditions that are with the bank that we are going to be dealing with, that is going to fund the transaction. And then after the clearing agent is done, the documentation we then need to submit this to the bank that will be funding and we would need approvals along the bank chain, that then eventually go to the Central Bank and are also captured into the Central Bank and approved from that end, and then it comes back to your bank and then comes back to us, which we then share with our clearing agent to go ahead with the process of bringing in the product. (Executive: Mozambique)

Table 2 highlights the typical time reported by the different executives to obtain short-term capital.

Although all the executives were asked to discuss the time needed to obtain short-term capital locally and abroad, many of them did not answer the question for foreign capital. Instead, they explained either the various obstacles preventing them from obtaining such funding in the first place, or its very high cost. Clearly, the long time it took to obtain the funding was not their central concern. In contrast, obtaining offshore capital in Botswana took a relatively short time. Botswana is a small market, but well-developed relative to other African countries, and many African firms direct foreign payments through Botswana.

Executives reported an even more complex situation for long-term capital. Long-term funding was hardly available locally, was for very short periods, and often in formats that would not be regarded as real long-term funding, like vehicle asset financing. Borrowing foreign currency from commercial banks was extremely expensive, and development finance institutions often the only resort. Even so, the cost of funding was extremely high. Table 3 summarizes.

Very few of the African financial institutions could provide long-term capital, and to get long-term capital from abroad introduced complications around scarce foreign currency. This situation forced executives to make what they knew to be suboptimal choices:

The cost of long-term funding, you still have it [interest] sitting somewhere around 14 to 15 percent. On the US Dollars. That’s steep. And then when you want to look at, okay, so the repayment period, the payback period, the IRR for that asset – the project then becomes very unattractive. So then it now becomes a case: Is it table stakes or is it something that is a need? If we can do without, you will have to put it aside. But then there are inefficiencies that you will be generating within the system if you don’t modernize your systems, you know. The inefficiencies that come with old machinery will also start kicking in on your business. […] For example, you still run with a machine that’s doing 40 times a day when if you had modernized a part of that machine, it was going to be running you 80 times a day. (Executive: Zimbabwe)

It is important to note that the interest rates reported do not represent the only costs payable by the firm.

There would be costs related to registering these applications, there would be also commissions which you pay upfront, fees for you to be able to get this disbursement. So when you look at all those costs, these are costs which are not there but when you add up then they become too much into the business and your cost of funding at the end of the day will go up, because of those unseen regulatory requirements. You have deposits, you are required to meet the professional – the legal fees, and therefore along the whole approval and application process, those costs add up to significant amounts. (Executive: Tanzania)

How Does This Happen?

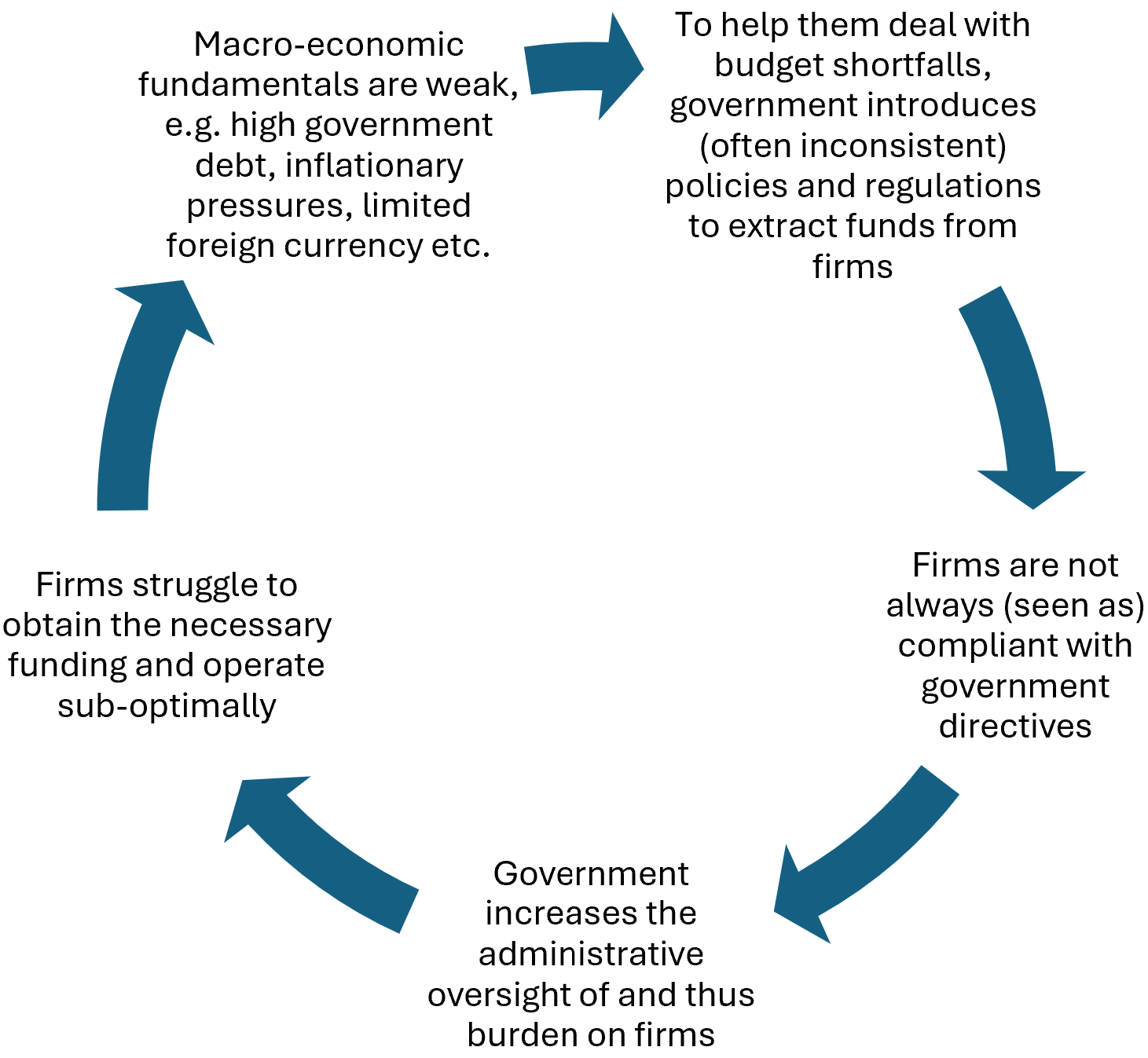

It is clear that Africans pay dearly for basic and inefficiently delivered access to capital. How does this happen? The explanations of the executives and of the various bank managers were aligned, and point to a vicious cycle, shown in Figure 1. First, the macro-economic fundamentals are weak. High government debt, inflationary pressures, limited foreign currency and others are constantly putting pressure not only on firms, but also governments. In response, executives explained, governments look to firms – especially larger ones like local MNEs – to help them manage these weaknesses. But government directives to extract funds are often inconsistent, and firms are not always (seen as) compliant with these changeable policies and regulations. Thus, the administrative “oversight” and burden on firms are increased.

Weak macro-economic fundamentals pose a big challenge. In Zimbabwe, the government has stated its intent to de-dollarize by 2030, effectively placing a ceiling on any borrowing post 2030. High inflation and weak currencies both present challenges:

There is just the uncertainty in terms of the economy, where people are not certain where the economy is heading in terms of the exchange rate. You do not know where it will be in a year or so, because in the past we’ve had significant devaluations overnight. The currency devalued by 44% and that would have been after another 25% devaluation a few months back. So there is that uncertainty where people generally trade with caution. And if it’s anything which is foreign currency denominated, then people are really cautious, and sometimes the funding becomes expensive. (Executive: Malawi)

In some cases, governments try to safeguard currencies, but the foreign currency shortages that result from having an artificially high currency give rise to parallel (black market) currency markets. Governments often respond to such issues by intensifying “oversight”, which involves cumbersome bureaucracy. Although initiated by regulatory requirements, their execution is cascaded to firms via banks.

It can take as long as three months because of course the banks have various credit committees and so on. They also have a lot of KYC’s [Know Your Customer] that the company has to submit which are quite rigorous, I must say. Then you see that the time frame to tick all the boxes in terms of getting approvals can take as long as three months. Even if you are simply doing a renewal, you know you’ve been borrowing from the same financial institution for five years, but you always come back to say it’s going to take at least three months to get it done. (Executive: Zambia)

A process that already takes long is further complicated by the inconsistent policies of governments, as the requirements for raising funding may well change before it is concluded. The executive from Zimbabwe commented that “you’re always on the lookout for a new policy statement, almost every two weeks”, and the Kenyan executive explained how that affected their ability to raise funds:

You know we are expecting around 9 to 12 months for us to raise a long term funding because the requirements keep on changing, and adding the information that the bankers keep on asking, up-to-date information. Like the information we submitted in March, management accounts, be it cash flow forecast, so they now [September] continue to ask for updated information in lights of the monetary and fiscal policies that are being announced by the government. (Executive: Kenya)

The one noteworthy exception was Botswana, and the financial intermediaries confirmed that Botswana was seeing increased business from across the continent. Against the backdrop of the experiences in the other countries, the shift is hardly surprising:

On the Botswana market, like I’ve said before, there isn’t really a lot of regulations that will end up affecting the long-term funding or capital requirement. No exchange controls, it’s easy to access both local and foreign currency, so there isn’t really much that really affects access to long-term capital. (Executive: Botswana)

What Should Managers Do?

Even assuming that our interviewees accurately identified the challenges, executives accurately alone cannot address the underlying turbulence and uncertainty facing African businesses. It is necessary to undertake policy reforms that improve policy consistency and certainty, reduce the “policing” of capital markets, offer greater independence of financial regulators like Central Banks, and align with international benchmarks in global financial markets. At the same time, African firms cannot wait with operating – and raising capital – until Africa is better governed. This leaves us with the question of what managers can and should do to finance their operations.

We suggest that dealing with this issue is only partly a question of managing finances through careful financial structuring. Managers in African firms also need to develop their people and even manage operations in such a way that they can meet their funding needs. Table 4 summarizes our recommendations.

When it comes to developing people to support financing needs, it is firstly necessary for managers inside the country to realize that they need to be actively thinking about and experimenting with different means of getting the necessary funding. Second, the knowledge gap between advanced economies and Sub-Saharan Africa with regards to product knowledge on financial instruments must be narrowed. Training for key employees involved in capital raising should include an overview of financial market instruments, and best practice in financial and capital markets. The financial instruments covered should include elements like the securitization of debtors’ books, and hedging of key risks associated with running a business.

Operations should also be managed in such a way that they assist in securing funding. If the transfer risk for repatriation of hard currency loan proceeds is high, either due to liquidity challenges or stringent regulations towards foreign currency, it is advisable to focus on local currency funding from the domestic market of the operating entity. MNEs often reinvest earnings back into the host country rather than seek repatriation. This choice is shaped by the geopolitical environment within which the MNE operates (UNCTAD, 2024); if the reinvestment were to yield good returns, the MNE is actually increasing the challenge of repatriating earned funds in the future. But provided that an MNE sees itself operating in a given location long-term, earned income is an attractive option for funding operations.

Prioritizing exports is another way to secure funding. Repatriating earnings from other African countries with liquidity issues tends to cause issues rather than help resolve them, but export earnings, specifically to outside of Africa, can be used to provide access to foreign exchange. Although many African countries allow a firm to offset only a proportion of foreign earnings against foreign expenses, many respondents mentioned the value of securitizing its exports.

Firms are also advised to implement a robust ESG (Environment, Social & Governance) policy. Numerous development financial institutions and commercial bank executives underlined that reasonably priced capital is available for African firms that are ESG compliant. Given concerns about weak governance in Africa, a better understanding of governance-related issues is especially important.

When it comes to structuring financial arrangements, it is advisable to have a flexible funding structure that allows a firm to switch between local and foreign currency funding options as far as possible. Another major recommendation is to centralize treasury operations into a country with favorable conditions for raising capital. This recommendation, consistent with the findings of Birkinshaw et al. (2006) that MNEs sometimes relocate corporate activities to more suited locations, allows the parent to help facilitate access to capital. In the case we investigated, and as per the financial intermediaries we interviewed, Botswana was increasingly hosting the finance function.

Conclusion

Despite the challenges they encountered, many of the respondents were optimistic about the prospects in Africa. One banker commented:

So Africa is a very exciting place at this point in time, on the rise, great opportunities. We see that the economy is growing, still continuing to grow at 5% plus on average. […] I think this is the only continent in excess of 4% GDP growth on a consolidated basis, where Europe might be sitting at 1.5% and Asia also. So all eyes are on this particular continent. And within African markets you see that there’s a whole lot of exciting economies, and very diversified in a bigger scheme of things. (Commercial bank executive: South Africa)

Much more work is needed to understand how MNEs seek to raise capital in Africa and how that affects them; whether they are from advanced or emerging economies, or are nascent MNEs. Understanding the challenges faced by nascent MNEs from other parts of the world is another important avenue for future research. Nonetheless, we believe that our work makes a useful contribution, offering practical ways to manage the challenges of raising capital in Africa. We hope that others find them of value.

Acknowledgements

We thank the individuals who had contributed to the data collection for their insights and feedback.

About the Authors

Helena Barnard (Ph.D. from Rutgers University) is full professor at the Gordon Institute of Business Science (GIBS), University of Pretoria. She is interested in how knowledge (and with it, technology, organizational practices and innovation) moves between more and less developed countries, particularly in Africa. She is the founding chair of the AIB Emerging Markets Shared Interest Group, and currently an area editor at the Academy of Management Perspectives and Journal of International Business Policy.

Samson Ruwisi has over 20 years of working experience in banking and commodity trading. He works in the field of treasury and trade solutions, structured trade and working capital, and structured project finance for corporates. He is a qualified banker with an MBA (Banking) from the University of London, and has completed his MPhil (International Business) at GIBS, University of Pretoria. He successfully completed the on-campus Global Executive Leadership Programme from Yale School of Management in 2024.