Introduction

While the latest World Bank Global Findex 2025 Survey Database shows that an additional 5 percent of adults globally benefitted from access to financial services between 2021 and 2024, most individuals, especially in Sub-Saharan Africa (20 percent) still remain without access to finance for economic exchange because of price and non-price barriers (Klapper, Singer, Starita, & Norris, 2025; World Bank, 2025a). Particularly, barriers such as costs, distance, and documentation requirements have led to lack of access to finance among the geographically dispersed economic agents in Africa. Yet proponents of the African Continental Free Trade Area (AfCFTA) have argued that the removal of barriers that limit trade activities can increase exchange of goods and services to spur economic integration within and across the continent.

The Global System for Mobile Communications Association (GSMA, 2024) suggests that the use of mobile phones, computers, and other digital technologies with internet connectivity, can remove access and usage barriers such as costs, distance, and documentation requirements that increase availability of finance for trade. More specifically, digital interoperability between the mobile money networks and digital payments system can allow traders to remotely gain access to timely finances to facilitate trade, especially in rural areas in Africa, where physical formal banks are absent (Okello Candiya Bongomin, Akol Malinga, Manzi, & Balinda, 2024). Mobile money networks and digital payments’ systems interoperability can offer better access to and usage of financial services to facilitate trade than the conventional banking system because of its wider coverage (Demirgüç-Kunt, Klapper, Singer, & Ansar, 2022; Okello Candiya Bongomin, Akol Malinga, Amani Manzi, & Balinda, 2023).

The existence of wider mobile money agent networks in most parts of Africa can also increase delivery of financial services to the geographically dispersed unbanked traders to conduct trade (Demirgüç-Kunt et al., 2022). Moreover, most small shops (“the dukas”) in rural parts of Africa that act as point-of-sale, have provided convenient platforms for mobile money transactions and digital payments to crowd-in more unbanked traders into the formal financial system. Kere and Zongo (2023) contend that digital payments through internet banking that reduce trade costs can stimulate trade growth prospects of AfCFTA by increasing exports among Intra-African traders.

Whereas mobile money and digital payments can allow the unbanked traders to access and use financial services remotely in the absence of banking infrastructures, there is need for interconnectivity between the mobile money networks and digital payments’ systems through account-to-account interoperability. Digital interoperability creates an intertwined settlement and clearing hub that promotes efficiency of digital transactions within the FinTech and National Payments’ ecosystems. This facilitates instant account-to-account and mobile wallet interactions and transfers to enable remote and convenient payments for goods and services by traders who do not have access to the physical formal banks.

Against this backdrop, there is need to advocate for digital interoperability to ensure on-time complete transaction cycle within the FinTech and National Payments’ ecosystems to make finance readily available to drive trade prospects in Africa. This article offers direction to trade policy in Africa to create a single unified digital market and favourable enabling environment for efficient functionality of digital interoperability within the FinTech and National Payments’ ecosystems in different countries in Africa to increase access to finance for trade to accelerate economic integration within and across the continent.

Global Trends in Digital Interoperability

According to the Global System for Mobile Communications Association (GSMA, 2024), mobile money networks and digital payments’ systems interoperability is when users of one mobile money service can transfer or make payments to another mobile money provider domestically or across borders between mobile money services and banks.

The interaction between the mobile money system and banks creates a transaction settlement and clearing platform that helps to strike a balance between the demand and supply of money. This determines the amount of money received and transferred between mobile money and bank accounts-to-accounts inter network transfers to instantly meet the demand and supply of money for trade.

Notably, the vertical and horizontal interoperability that link the mobile money operators’ networks, platforms, agents, merchants, and data, can promote instant access to financial services domestically and internationally through account-to-account (A2A) transfers at reduced costs due to seamless and effective interconnectivity (GSMA, 2024).

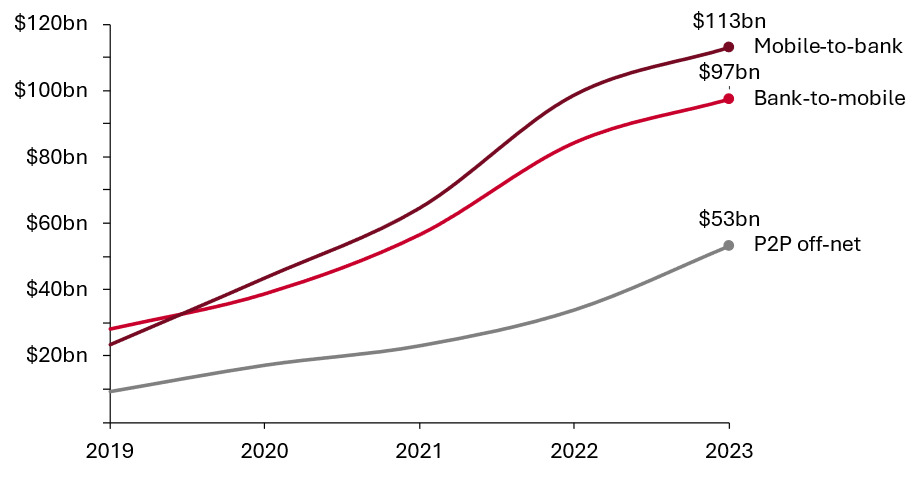

The global (Africa inclusive) digital interoperability transaction values between mobile money financial services and banks grew to over $113bn in mobile-to-bank transfers with more than $97bn in bank-to-mobile transfers and about $53bn in P2P (Person-to-Person) off-net transfers in the periods 2019 to 2023 as shown in Figure 1.

Financial Inclusion and Trade in Africa

An inclusive financial system facilitates efficient allocation of productive resources that can potentially reduce the cost of capital for trade (Cama & Emara, 2022). The availability of a wide range of financial services is very vital for the economic well-being of individuals (World Bank, 2024).

Financial inclusion means the ability by individuals and businesses to have access to useful and affordable financial products and services such as savings, credit, payments, and insurance that are relevant and suitable to them (World Bank, 2025b). Access to affordable and timely financial services helps economically active agents to generate income through trade (Okello Candiya Bongomin, Chrysostome, Nkongolo-Bakenda, & Yourougou, 2024). Universal financial inclusion enhances efficiency and welfare by providing avenues for secure and safe saving practices to accumulate money for trade.

The main goal of the AfCFTA is to increase trade and economic integration by removing trade barriers to promote free movement of people, capital, and investments through creating a single market for goods and services across Africa and beyond. Nevertheless, the micro, small and medium enterprises engaged in trade in Africa and other emerging markets experience over a $1.1 trillion financing gap yearly because of absence of suitable banking infrastructures (Beck, 2023; World Bank, 2024). This has greatly affected local and cross border trade, especially in Africa.

By leveraging on digital interoperability, traders in Africa and beyond can use mobile money and digital payments over the internet to gain access to convenient and affordable finance to pay for goods and services. On the other hand, while this is possible, digital interoperability functionality could be limited by a high tax burden on businesses, gender bias, urban and rural divide, lack of identification documentation for SIM card registration, high interest rates on digital loans, difficulties in verifying credit worthiness of digital borrowers, difficulties in monitoring and enforcing digital loan repayments, lack of standardized digital protocol and compatibility of digital regulations and laws, limited digital skills, and limited financial knowledge and skills, among others. These limitations have affected digital interoperability functionality as highlighted in Table 1.

Digital Interoperability and AFCFTA Trade Prospects

According to Coye and Loftesness (2013), digital interoperability refers to account-to-account (A2A) transfers between customer accounts at different mobile money schemes and between accounts at mobile money schemes and accounts at banks.

The African Union Commission defines the African Continental Free Trade Area (AfCFTA) as a free trade agreement that covers most of Africa aimed at removing barriers to trade and eliminating tariffs on goods and services to increase socio-economic development, reduce poverty, and make Africa more competitive in the global market. The AfCFTA advocates for removal of trade barriers to promote exchange of goods and services within and beyond Africa through formation of a single market regime. Whilst the formation of AfCFTA is a landmark initiative towards boosting intra-Africa trade volumes, there were no defined banking infrastructures available to meet the financial needs of the unbanked traders at the inception of this noble trade initiative.

Digital interoperability can offer the channel through which traders can gain access to and usage of financial services. Digital interoperability ensures that the mobile money providers’ bank accounts have money readily available that is remitted into the mobile wallets of traders to meet on-time electronic money requests and transfers to enable them to conduct trade. This is driven by instant information exchange and coupling grounded in the formal theory of interoperability of systems supported by a harmonized single digital market regime and legal framework (Diallo, Herencia-Zapana, Padilla, & Tolk, 2011).

Mobile money networks and digital payments’ systems interoperability that ensure customer data protection can offer convenient, secure, private, and affordable access to financial services through registered Subscriber Identity Module (SIM) and Personal Identification Number (PIN) not readily available from the traditional banks for trade (Okello Candiya Bongomin, Akol Malinga, et al., 2024). The A2A interoperability can also increase access to and usage of financial services by unbanked traders to perform transactions because it is faster due to high-speed broadband and wider coverage (Suri et al., 2023). The bulky transfers of money electronically through digital interoperability can enable unbanked traders to easily access finance to make timely payments for goods and services from suppliers. This can sustain good trade relationships between the traders and suppliers (Domingo, Arnold, & Apiko, 2023).

Mobile money networks and digital payments’ systems interoperability can further help traders to easily access loans to pay for goods and services. The quick digital loan approval process based on the digital credit history and transaction trails of traders backed by strong credit bureau customer data sharing can make money instantly available for trade (Björkegren, Blumenstock, & Folajimi-Senjobi, 2022). Mobile money networks and digital payments’ systems interoperability through unified digital platforms can also allow traders to raise funds through peer-to-peer lending and online crowdfunding for trade (Halim, 2024). The use of online platforms to source financing makes funds available to pay for goods and services to sustain trade (Okello Candiya Bongomin, Yourougou, & Munene, 2020).

The existence of an efficient digital interoperability system that ensures on-time availability of finance can allow traders to easily transact in the market in Africa and beyond. This can promote and sustain trade to accelerate economic integration among African countries.

Policy Implications

This article articulates how mobile money networks and digital payments’ systems interoperability grounded in the Formal Theory of Interoperability of Systems can offer on-time availability of finance to facilitate trade in Africa. Accordingly, the highlighted recommendations in the Table 2 could be useful for progress of trade prospects of the African Continental Free Trade Area.

Conclusion

Digital transformation through digital interoperability has potential to foster sustainable development by enhancing regional connectivity and a unified single digital market that could redefine Africa’s future trajectory and role in the global economy through increasing trade.

Digital interoperability is more convenient for traders because it allows access to customers outside the digital providers’ networks. Specifically, mobile money and digital payments can lead to more inclusive digital economies by expanding access to account-to-account payment systems that make funds more available, secure, and traceable to support progressive trade activities.

The use of digital interoperability can allow more funds to enter into the digital financial ecosystem to facilitate trade. This helps traders to have enough funds that are digitally remitted to pay for goods and services rather than using cash that may delay distant transactions. In a nutshell, digital cash can efficiently facilitate both local and cross-border exchanges more than physical cash.

Nonetheless, while the importance of digital interoperability cannot be overemphasised, system redundancy and outages during operation may affect the efficiency of mobile money and digital payments. More so, while some governments have revised the taxes on digital financial transactions, most subscribers still find it expensive. Similarly, high interest rates on digital loans remain an obstacle in digital borrowing among many prospective traders.

Finally, culture as a strong contextual factor has resulted in persistent digital divide in the digital age. This has affected widespread mobile phones and SIM ownership in Africa, especially by women. Future studies are inevitable to further investigate how these factors could influence digital interoperability and trade prospects in Africa with reference to the novel AfCFTA initiative.

Acknowledgements

The authors are forever grateful to the Editor-in-Chief, Special Issue Editorial team, and anonymous reviewers for the insightful comments provided to improve the quality of this paper to publishable standard of the Journal. The efforts of all authors of this article are also duly acknowledged.

About the Authors

George Okello Candiya Bongomin holds a Ph.D in Finance and based at the Faculty of Graduate Studies and Research and Finance Department, Faculty of Commerce, Makerere University Business School, Kampala Uganda. Currently, he is Visiting Professor and Scholar at the Laboratory for Financial Engineering at Laval University, Hill and Levene Schools of Business at University of Regina, Ivey Business School of Western University, and State University of New York (U.S.A). He is corresponding author of more than 50 articles in Banking and Finance Journals like Managerial Finance, International Journal of Bank Marketing, Journal of Financial Regulation and Compliance, Information Technology and People, Social Responsibility Journal, Journal of Small Business and Enterprise Development, Cogent Economics and Finance, International Journal of Sociology and Social Policy, Journal of African Business, and Digital Policy, Regulation and Governance among others. His research interests are in financial inclusion, artificial intelligence/machine learning and financial services, digital financial services, microfinance, behavioral finance, entrepreneurship, banking and finance practice, institutional economics, financial consumer protection, ESG (Environmental, Social and Governance), green finance/climate change financing, and business psychology.

Elie V. Chrysostome is Professor of International Business at Ivey Business School of Western University in Canada and Editor-in-Chief of Journal of Comparative International Management (JCIM). He previously taught at Laval University (Canada), University of Moncton (Canada) and at The State University of New York (USA). He is author and coauthor of more than 50 publications in various journals including Journal of International Business Policy, Thunderbird International Business Review, Journal of International Entrepreneurship, Journal of Small Business and Entrepreneurship, Journal of African Business. His research interests include Immigrant & Transnational Diaspora Entrepreneurship, Foreign Direct Investments (FDI) in Emerging Markets, impact of sanctions on MNEs in Africa, and Capacity Building in Africa.

Michael Atingi-Ego is Governor at the Bank of Uganda, Kampala Uganda. He holds a Ph.D in Economics from Liverpool University, a MSc. Economics in International Economics and Banking from Cardiff Business School, University of Wales, and a BSc. Economics from Makerere University. Previously, he served as the Deputy Governor at the Bank of Uganda, Executive Director of the Macroeconomics and Financial Management, Institute of Eastern and Southern Africa (MEFMI), based in Harare, Zimbabwe. His research interests are in macroeconomics, financial policies, and statistics.

Pierre Yourougou is Professor of Banking and Finance. He is Deputy Director General of the National Polytechnic Institute Felix Houphouet-Boigny, Cote d’Ivoire in charge of Research, Innovation and Technopole. He has more than 30 years of teaching experience at different schools in North America, Asia and Africa. His research interests are in financial inclusion, development finance, banking and finance, and international business.