Introduction

When the Russian army invaded the Ukraine on February 24, 2022, the managers of firms doing business with Russia witnessed the escalation of rising tensions between Russia and the NATO bloc countries into a dangerous crisis. The possibility of a catastrophic total war between the world’s military powers resulted in many of the countries opposing Russia to engage in economic warfare, involving the use of sanctions, the freezing of Russian assets, and the pressuring of MNEs to divest. However, while there is a strong moral imperative upon which many managers are choosing to act by withdrawing, the demand for firms to participate in economic warfare can be carefully balanced with decisions that maintain strategic flexibility and retain the option for continuing business in Russia in the present and future. Other recent studies have provided insights into how MNEs can assess their exposure to geopolitical conflicts (De Villa, 2023), identify the operational and reputational drivers of MNE responses to such conflicts (Mol, Rabbiosi, & Santangelo, 2023), and even contribute to peace-building efforts in the midst of conflict (Melin, Sosa, Velez-Calle, & Montiel, 2023). The insights offered in this paper aim to provide practitioners with an awareness of the range of options to remain in the midst of geopolitical crises, specifically highlighting strategies that involve localizing operations and leveraging home country neutrality to forgo the need to permanently exit the market. Moreover, these insights point to strategic steps MNEs can take to build resilience in the event of future crises in potentially volatile host countries.

These insights are grounded in a unique combination of sources, first drawing upon references to business historical research considering MNE decisions in previous periods of global crisis (e.g., WWII), and then analyzing the decisions of foreign firms to withdraw from or remain in Russia based on data currently being collected as the war unfolds (CELI, 2022). Accordingly, this paper also sheds light on the value of looking at historical cases to inform our interpretations of still-unfolding events that involve the complex interplay of the geopolitical context and firm-level strategizing (Welch, Paavilainen-Mäntymäki, Piekkari, & Plakoyiannaki, 2022).

MNEs, Geopolitics, and History

Looking at IB history can provide a font of insights for how MNEs managed their foreign operations in contexts made extremely risky by the escalation of tensions between large, global powers (Casson & Lopes, 2013). Notably, the period of the 1930s and 1940s has featured prominently in recent business historical research on MNEs and geopolitical risk. When the German army invaded Poland on September 1, 1939, the combatant countries moved to confiscate the assets of each other’s MNEs. Anticipating confiscation, many German MNEs had implemented attempts to cloak their home-country identity, often to the dissatisfaction of the Nazi regime, by developing complicated ownership structures through non-aligned countries, such as Switzerland (Kobrak & Wüstenhagen, 2006). These efforts often failed, resulting in the seizure of these MNEs’ foreign assets and, as exemplified by the German personal-care products company Beiersdorf, greater difficulty in recovering assets in the post-War period (Jones & Lubinski, 2012).

For MNEs from Allied countries doing business in Axis countries and their occupied territories, remaining in enemy territory involved the localization of control, even if the subsidiaries continued under the foreign firm’s ownership. Well-known cases of major MNEs, such as Ford, General Motors, and Royal-Dutch Shell in Germany, demonstrate how the operations of these companies were placed under the control of local managers and supported the Nazi war effort (e.g., Boon & Wubs, 2020; McCraw & Tedlow, 1997). In this way, essentially through a decoupling of control between the home-country headquarters and their host-country subsidiaries, these firms contributed to the war efforts of both sides of the conflict but retained the option to retake control of their foreign operations after the conflict was over.

MNEs from countries adopting a neutral stance in the conflict also developed localizing and cloaking strategies, but with the added benefit of leveraging their neutral status to avoid being treated in the same way as firms from combatant countries. For instance, Nestlé relied on Swiss neutrality to bolster the resiliency of its operations in Japan (Donzé & Kurosawa, 2013). MNEs from Nazi-occupied countries, seeking to avoid being associated with the Nazis, attempted to leverage their neutrality to avoid repercussions for their operations in Allied and other risky countries. For example, the Danish construction company Christiani & Nielsen localized its operations in Latin America and emphasized the de facto neutrality of Denmark to counter its ‘blacklisting’ by the Allied governments (Andersen, 2009); similarly, the Australian subsidiary of the Dutch electronics MNE Philips had to develop strategies to mitigate the suspicions of Australian intelligence agencies (van der Eng, 2017).

For the important question of whether to withdraw or remain during geopolitical crises, these historical cases point to a valuable insight: while the conflict challenged the ability of MNEs to continue business as usual, they employed strategies – specifically, localizing their operations and leveraging their home-country neutrality – to position themselves advantageously during and after the conflict. Accordingly, when considering the contemporary case of foreign firms in Russia, we would expect to find similar patterns.

Withdraw or Remain: Decisions by Foreign Firms in Russia

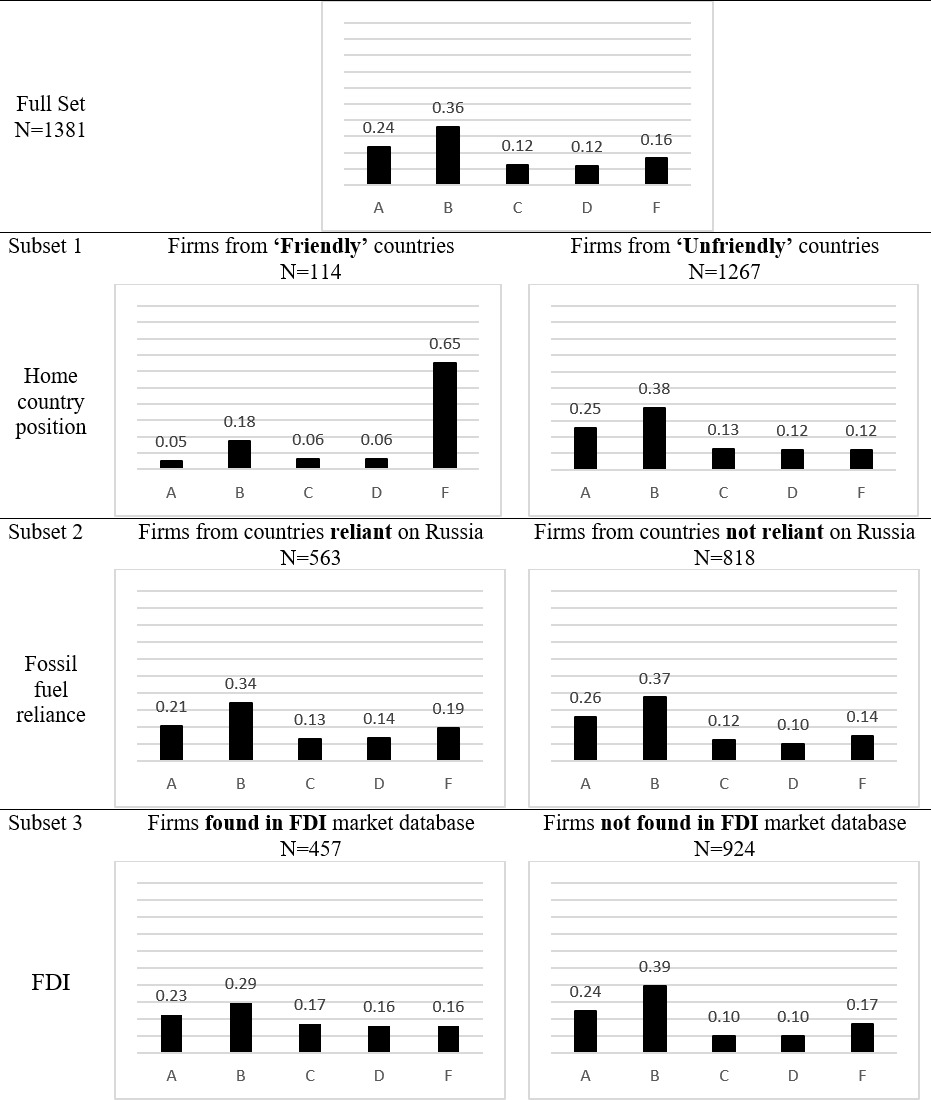

Indeed, turning to the current challenges MNEs are facing because of the Russian invasion of Ukraine, the lessons from history assist in interpreting how, despite the position of an MNE’s home country in the conflict, firms can employ strategies which avoid permanent exit from the market and, instead, retain options to continue business. A valuable resource of information detailing the decisions by 1381 foreign firms from 67 countries to remain in or withdraw from Russia is the result of ongoing research being carried out at the Yale School of Management (CELI, 2022). Significantly, the database classifies firm decisions into one of five distinct categories capturing the range of options for firms, and these are labelled with grade levels A (withdrawal), B (suspension), C (scaling back), D (buying time), and F (digging in), which, for the data collector, carry an evaluative judgement intended to pressure firms to withdraw. Table 1 details this range of decisions, also providing the total number of firms in the database which have made each decision as of December 2022.

While the decisions to withdraw and suspend operations dominate among firms reported in the CELI database, a comparison between several subsets reveals both firm- and home-country-level factors which result in a greater likelihood of choosing options to remain. Table 2 compares the distribution of decisions depending on whether the MNE’s home country is on Russia’s list of ‘unfriendly’ countries (Al Jazeera, 2022), whether the MNE’s home country is heavily reliant on Russian fossil fuel imports (International Energy Agency, 2022), and whether the MNE is found in a database of firms having made greenfield foreign direct investments in Russia in the past 20 years (Financial Times, 2022).

Unsurprisingly, firms from countries not labelled ‘unfriendly’ by Russia continue operations at a very high rate. These ‘friendly’ nations include both countries allied with Russia, such as China (Gabuev, 2022), and neutral countries attempting to take on a diplomatic role in the conflict, such as Turkey (Kusa, 2022). Accordingly, under the cover of neutrality, we observe firms leveraging their home country’s position to maintain business-as-usual. For example, in contrast to other airlines such as Lufthansa, Austrian Airlines, and KLM-Air France, who made the easily reversible decision to temporarily halt all flights to and from Russia, Turkish Airlines continued serving its destinations inside Russia. Similarly, while the alcoholic beverage manufacturers Carlsberg, Heineken, and others abandoned significant foreign direct investments in the Russian market, Turkish brewer Anadolu Efes continued bottling at its plant in Russia to serve what is one of its key markets. By utilizing the cover of a favorable home-country position, such as neutrality, some MNEs can expand their competitive position in the market which others decided to exit.

Countries labelled by Russia as ‘unfriendly’ may still vary in how confrontational they approach relations with Russia, especially those countries with a heavy reliance on Russian fossil fuels. The comparison in Table 2 indicates that firms from countries more reliant on Russian oil and natural gas have a slightly higher frequency of choosing options to remain. After both BP and Shell decided to divest from their respective engagements with Russian partners Rosneft and Gazprom, the French oil company Total Energies resisted significant divestments (Kostov, 2022), given it has heavily invested in Russia since 1991 and, according to the FDI markets database, had made capital investments totaling nearly $3.5 billion since 2003. The attempts of French President Emmanuel Macron to mediate a dialogue with Russian President Putin also reinforce a more neutral positioning of France in the conflict that Total has seized upon, in contrast to some of its major competitors from other European countries. The greater dependence of many European countries on Russian energy has manifested in decreased pressure for firms to participate in economic warfare, opting instead to avoid Russia’s economic backlash and assert neutrality through continuing operations and maintaining control of key assets.

Total’s resistance to withdraw from its Russian investments also reflects how firms with significant foreign direct investments will seek to maintain their business in Russia and retain options to restart business-as-usual in the future. The final comparison in Table 2 shows that firms found to have greenfield investments in Russia are much more likely to continue business with little interruption, even if there are significant pressures from their home countries to divest. Indeed, for the subset of firms found in the FDI database, the average total capital investment corresponding to each of the ‘exit’ decisions indicates this trend: firms choosing option A – withdrawal (average $289 million); option B – suspension ($255 million); option C – scaling back ($377 million); option D – buying time ($291 million); and, option F – digging in ($188 million). Cognizant of having significant investments at stake, some firms opting to suspend operations have done so through a deliberate strategy of using local partners to steward their investments temporarily. For example, Ford’s decision to temporarily withdraw from its joint venture with Sollers comes with the 5-year option to repurchase its shares in the partnership, the operations of which will continue even without Ford’s participation for the time being (Ford, 2022). Others, such as the tire-manufacturer Michelin, opted to transfer control to their existing local management. This localization strategy, which is especially valuable for firms that had already established local partners, combines the dual benefits of demonstrating a strong economic response (i.e., market exit), while allowing operations to continue under local management until the conditions for re-entry are more favorable.

Geopolitics and MNEs: Past and Present

What history and our present circumstances show us is how the position of an MNE’s home country in an international geopolitical crisis can have powerful influence on the MNE’s decisions whether to stay or go in hostile host countries. However, the evidence also shows that MNEs have often resisted the intentions of their home country by choosing to maintain their host-country operations to some extent or exit in a manner that retains options for re-entry. I have shown how an analysis of certain country- and firm-specific factors can assist managers to reach a decision that can satisfy key stakeholders, while avoiding complete abandonment of the host country. Figure 1 depicts a series of actionable decisions based upon the characteristics of a firm’s home-country geopolitical position (vis-à-vis the host country) and the extent of its investment in the host country. The flow of this diagram assumes that, absent the legal and moral imperatives generated by the geopolitical crisis, MNEs would prefer to continue business in the host country either now or in the future. Additionally, each strategic decision for remaining and withdrawing carries both advantages and disadvantages, which managers need to balance against the long-term interests of their firm and its operations in the host country.

Crucially, the country- and firm-specific factors considered here and the associated decisions recommended to MNEs based upon those factors reveal important considerations for multinational managers who may encounter new geopolitical crises in the future. For instance, if MNEs from countries adopting a more neutral stance can use their neutrality as a cover for continuing operations, gaining an advantage over competitors who withdraw from the market, and mitigating scrutiny from both home- or host-country stakeholders, it would be sensible for MNEs to encourage home-country neutrality in future conflicts. Nonmarket strategies involving the lobbying of home-country governments or the diplomatic brokerage of home-host relations could help foster a neutral positioning before geopolitical tensions escalate into crises. Similarly, if heavily-invested MNEs can opt for strategies that utilize local partners to steward their operations temporarily, providing a means to exit the market while retaining the option for re-entry, it would behoove MNEs, especially those with significant investments in potential geopolitical hotspots, to forge stronger relationships with local partners and enhance the capabilities of local management to operate autonomously. In both instances, these insights can point managers towards strategies that build resilience in their organizations abroad in the event of future crises.

About the Author

Thomas DeBerge is a doctoral student in the Department of Business Administration at the Gies College of Business, University of Illinois at Urbana-Champaign. His research focuses on the strategies of MNEs for managing the nonmarket environment, especially environments marked by contentious political conflict and competition between political actors. He seeks to enrich his research through the use of novel data and mixed-methodological approaches including business history and quantitative analyses.